This is fantastic news for anyone dreaming of homeownership or looking to refinance: the 30-year fixed mortgage rate has significantly dropped by 45 basis points compared to last year, according to the latest data from Freddie Mac, making buying a home much more achievable this spring.

While rates did tick up slightly this past week to 6.22%, it’s crucial to zero in on what that year-over-year comparison tells us. The current average is a full 45 basis points lower than the 6.67% average recorded during the same week last year. This isn’t just a small blip; it’s a substantial shift that could put homeownership within reach for many more people this spring.

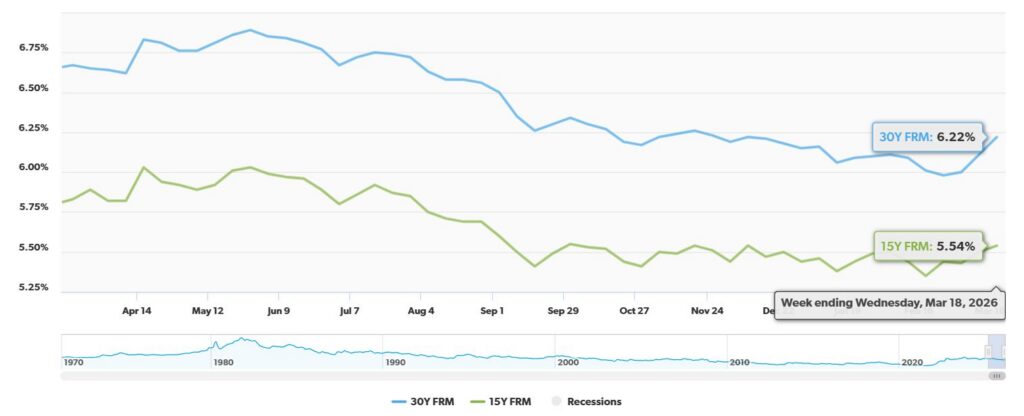

30-Year Fixed Mortgage Rate Drops Steeply by 45 Basis Points

For those who aren’t immersed in mortgage lingo every day, a “basis point” might sound a bit technical. Think of it this way: one basis point is equal to 0.01%. So, a 45 basis point drop means the interest rate has fallen by 0.45%. It might not sound like a huge number in isolation, but when it comes to mortgages – especially a long-term one like a 30-year fixed – this difference can translate into significant savings over the life of the loan.

As Freddie Mac’s Primary Mortgage Market Survey® highlights, as of March 19, 2026:

- The 30-year fixed-rate mortgage (FRM) averaged 6.22%.

- This is a slight increase of 0.11% from the previous week’s 6.11%.

- However, and this is the crucial part, it’s a notable 0.45% lower than the 6.67% seen a year ago.

This difference, while seemingly small on a week-to-week scale, represents a real opportunity for buyers. What I’ve seen in my years working with the housing market is that even small decreases in interest rates can make a big impact on what people can afford.

A Deeper Dive: How This Affects Your Wallet

Let’s crunch some numbers to see the real-world impact of this rate drop. When considering a mortgage, the interest rate is a major factor in your monthly payment. A lower rate means a lower monthly payment, freeing up your budget for other expenses or allowing you to afford a slightly larger home.

Consider this comparison for a 30-year fixed-rate mortgage, using the current rate of 6.22% versus last year’s average of 6.67%:

| Loan Amount | Monthly Payment (6.22%) | Monthly Payment (6.67%) | Monthly Savings |

|---|---|---|---|

| $300,000 | $1,841.30 | $1,929.87 | $88.57 |

| $450,000 | $2,761.95 | $2,894.80 | $132.85 |

| $600,000 | $3,682.60 | $3,859.74 | $177.14 |

Looking at these figures, even on a $300,000 loan, you’re saving nearly $89 a month. On a larger loan, like $600,000, that monthly savings jumps to almost $178. Over 30 years, this adds up to thousands upon thousands of dollars in savings. This is the kind of difference that can help someone get approved for a mortgage they might have been denied previously, or allow them to buy a home that better suits their family’s needs.

Beyond the Weekly Wobble: The Bigger Picture of Affordability

It’s easy to get caught up in the week-to-week fluctuations of mortgage rates. The fact that rates have edged up slightly this week is not uncommon. The market is influenced by a lot of factors, from inflation numbers to Federal Reserve policy, and it can be a bit of a rollercoaster. However, as Freddie Mac’s Chief Economist, Sam Khater, points out, “the market is more affordable than last spring.” I completely agree with that sentiment.

We’ve seen periods where rates flirted with or even exceeded 8% in late 2023. Compared to those highs, the current average of 6.22% is a significant improvement. This sustained dip from last year, despite short-term increases, paints a more optimistic picture for potential homebuyers. It means that while you might see small daily or weekly changes, the overall trend has been favorable for affordability.

This improved affordability is reflected in positive market indicators. We’re seeing improvements in purchase applications and pending home sales, which suggests that more people are actively looking to buy and are able to move forward with their plans. This is the kind of momentum that makes for a healthier and more dynamic housing market.

The 15-Year Fixed: Another Option for Savvy Borrowers

While the 30-year fixed-rate mortgage gets a lot of attention because of its lower monthly payments, it’s always worth looking at other options. The 15-year fixed-rate mortgage also offers a compelling picture.

According to Freddie Mac:

- The 15-year fixed-rate mortgage averaged 5.54%.

- This is up slightly from 5.50% last week.

- However, it’s a 0.29% lower than the 5.83% average from the same week last year.

Borrowing on a 15-year term means you’ll have higher monthly payments compared to a 30-year mortgage, but you’ll pay significantly less interest over the life of the loan and own your home free and clear much faster. For those who can comfortably manage the higher payments, a 15-year mortgage can be a very smart financial move.

What Does This Mean for the Spring Homebuying Season?

This 45 basis point drop in the 30-year fixed mortgage rate is precisely the kind of good news that can energize the spring homebuying season. Buyers who may have been priced out or were hesitant due to high borrowing costs are now likely to re-enter the market.

Here’s what I believe this will translate to:

- Increased Buyer Confidence: With lower rates and a general sense of improved affordability, buyers will feel more confident making a purchase.

- More Competitive Market: As more buyers enter the fray, we might see increased competition for desirable properties. It’s important for buyers to be prepared and act decisively when they find the right home.

- Refinancing Opportunities: Homeowners who have been waiting for a better rate to refinance their existing mortgage could also find this a good time to explore their options. Lower rates can reduce monthly payments or allow homeowners to tap into their home equity.

It’s still important to remember that the housing market is local, and prices can vary significantly by region. However, this broad decrease in mortgage rates is a positive tailwind for the entire country.

🏡 Two Rentals With Strong Investor Potential

Pleasant Grove, AL

🏠 Property: 4th Ave (1549 sqft)

🛏️ Beds/Baths: 3 Bed • 2 Bath • 1549 sqft

💰 Price: $265,000 | Rent: $1,850

📊 Cap Rate: 6.2% | NOI: $1,368

📅 Year Built: 2026

📐 Price/Sq Ft: $172

🏙️ Neighborhood: B+

Pleasant Grove, AL

🏠 Property: 4th Ave (1856 sqft)

🛏️ Beds/Baths: 3 Bed • 2 Bath • 1856 sqft

💰 Price: $410,000 | Rent: $3,200

📊 Cap Rate: 5.8% | NOI: $1,981

📅 Year Built: 2026

📐 Price/Sq Ft: $221

🏙️ Neighborhood: B+

Two Pleasant Grove rentals—one affordable with higher cap rate vs one larger with stronger NOI. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Build Passive Income & Wealth with Turnkey Rentals

Mortgage rates remain near 6%, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

🔥 HOT INVESTMENT Properties JUST ADDED! 🔥

Request a Callback / Fill Out the Form Online

{kind=link}