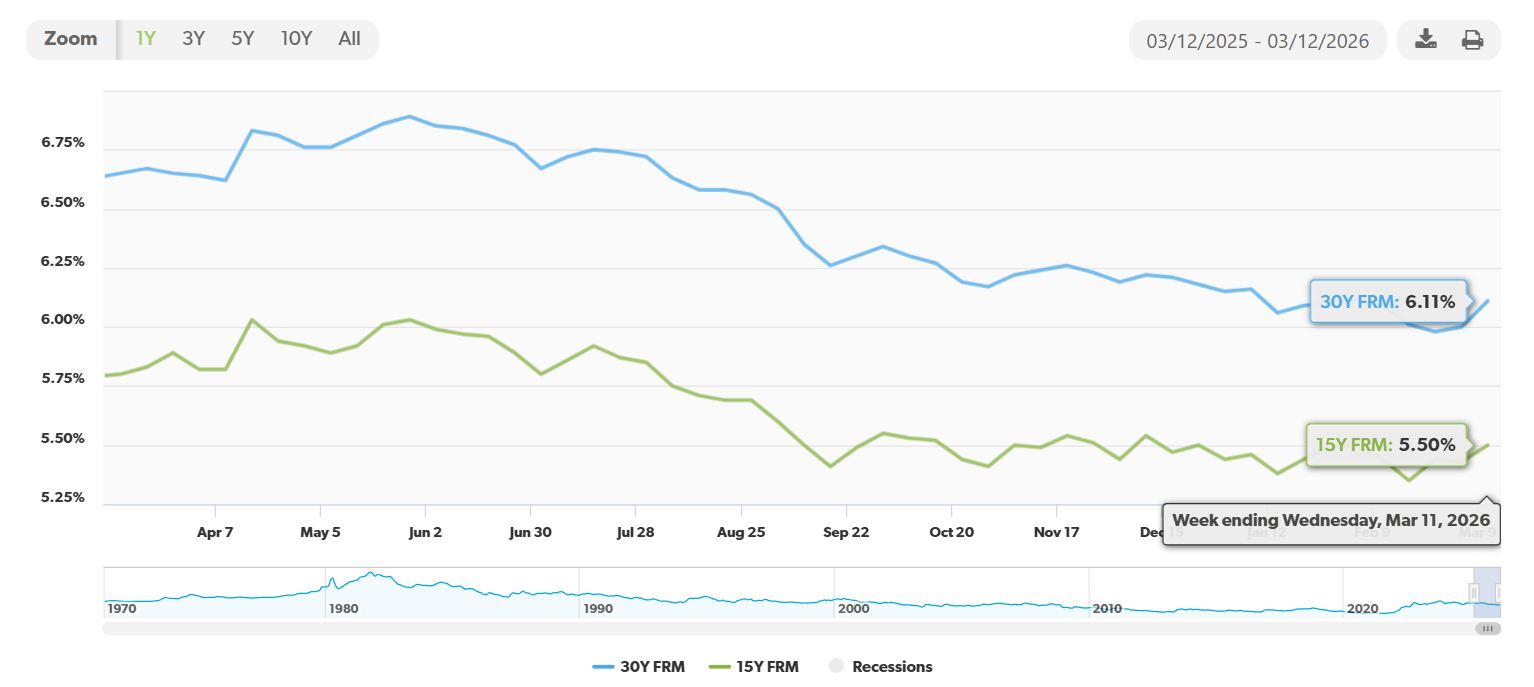

If you’ve been dreaming of owning a home or looking to refinance your current mortgage, I’ve got some welcome news for you. The average 30-year fixed mortgage rate has gone down by a significant 54 basis points compared to this time last year. This isn’t just a small blip on the radar; it’s a notable shift that could make a real difference in your homeownership journey. As of Freddie Mac’s Primary Mortgage Market Survey for the week ending March 12, 2026, the average reached 6.11%, a noticeable dip from the 6.65% we saw a year prior. It signals a potential shift that could unlock doors for many aspiring homeowners and provide relief for those looking to adjust their existing loans.

30-Year Fixed Mortgage Rate Drops Steeply by 54 Basis Points

What Exactly is a “Basis Point” and Why Does It Matter?

Before we dive deeper, let’s quickly clarify what we mean by “basis points.” Think of it like this: one basis point is equal to one-hundredth of a percent (0.01%). So, a drop of 54 basis points translates to a 0.54% decrease in the mortgage rate. While that might sound small, when you’re talking about the cost of borrowing hundreds of thousands of dollars over 30 years, that half-a-percent can add up to many thousands of dollars in savings.

The Numbers: A Clearer Picture of the Drop

Freddie Mac’s latest report provides some really valuable data, and I’ve put together a table to make it easy to see the changes. This isn’t just about a single week’s fluctuation; it’s about looking at the bigger picture, including comparisons to last week, last month’s average, and, most importantly, last year.

Here’s a breakdown from the Primary Mortgage Market Survey® for the U.S. weekly averages as of March 12, 2026:

| Mortgage Type | Current Avg. (03/12/2026) | 1-Week Change | 1-Year Change | Monthly Avg. | 52-Week Avg. | 52-Week Range |

|---|---|---|---|---|---|---|

| 30-Yr Fixed FRM | 6.11% | +0.11% | -0.54% | 6.03% | 6.44% | 5.98% – 6.89% |

| 15-Yr Fixed FRM | 5.50% | +0.07% | -0.30% | 5.43% | 5.66% | 5.35% – 6.03% |

Note on Savings: The most impactful saving comes from the 30-year fixed rate’s 0.54% year-over-year drop. Let’s look at an example for a $300,000 loan.

- At 6.65% (last year): Monthly Principal & Interest Payment = ~$1,943

- At 6.11% (this year): Monthly Principal & Interest Payment = ~$1,827

That’s a difference of $116 per month, or over $1,392 per year, in savings on principal and interest alone! Over the life of a 30-year mortgage, that’s tens of thousands of dollars back in your pocket. It’s this kind of tangible benefit that shows why tracking mortgage rates is so crucial.

Why the Recent Uptick Despite the Yearly Drop?

It’s important to note that while the year-over-year comparison is fantastic news, the rate for the week ending March 12, 2026 (6.11%) is slightly up from the previous week (6.00%). This might seem confusing, but it’s a common occurrence in the market, and Freddie Mac’s Chief Economist, Sam Khater, offers some insight.

He mentions that buyers are still responding positively to rates in this current range, which is why we’re seeing increased housing activity. Existing-home sales, for instance, went up 1.7% in February, and purchase applications have also seen an uptick as we head into the spring homebuying season. This resilience from buyers, even with minor weekly fluctuations, is a strong indicator of market health.

What’s driving these small weekly swings? Often, it’s a mix of factors. In this instance, economic news and global events can play a big role. The mention of “bond market jitters and inflation concerns stemming from the conflict in Iran” is particularly telling. Such geopolitical events can create uncertainty, leading investors to move their money, which in turn affects bond yields and, consequently, mortgage rates. It’s a reminder that the mortgage market doesn’t exist in a vacuum.

Homebuyer Resilience: A Sign of a Healthy Market?

I’ve seen many markets over the years, and what strikes me about this situation is the apparent resilience of homebuyers. Despite the temporary bumps, the fact that activity is picking up suggests that people are seeing value and opportunity at these current rate levels. The spring homebuying season is traditionally a busy time, and it seems like buyers are eager to take advantage of the still-lower rates compared to last year.

This upward trend in existing-home sales and purchase applications is exactly what I’d expect to see when rates have fallen significantly over a longer period. It’s not just about the week-to-week numbers; it’s about the sustained availability of more affordable financing.

Looking Back: A Brief Dip Below 6%

It’s also worth remembering that rates have recently touched even lower points within the past few months. The data indicates that rates briefly dipped below the 6% threshold in late February, reaching their lowest point in over three years at 5.98%. While we’ve seen a slight reversal since then, this demonstrates that even more favorable conditions have been within reach. This historical context is crucial for understanding the current market dynamics.

What This Means for You: Potential Impact on Your Homeownership Goals

So, what does this 54 basis point drop in the 30-year fixed mortgage rate really mean for you?

- For First-Time Homebuyers: This is a golden opportunity. The lower monthly payments can make a home more affordable, potentially allowing you to qualify for a larger loan or simply reduce your monthly burden, freeing up cash for other investments or expenses.

- For Current Homeowners (Refinancing): If you have an older mortgage with a higher interest rate, now might be the perfect time to explore refinancing. Even if your current rate isn’t extremely high, shaving off over half a percentage point can lead to significant savings over the remaining term of your loan. You can also potentially shorten your loan term or even pull out some equity for home improvements or other needs.

- For Investors: Lower borrowing costs can improve the cash flow on investment properties, making them more attractive.

It’s not just about the numbers on paper; it’s about how these changes translate into real-world financial benefits. My advice? Don’t just read the headlines; take the time to see how this affects your personal financial situation.

The Road Ahead: What to Watch For

While this recent drop is excellent news, the mortgage market is always influenced by a multitude of factors. We’ll need to keep an eye on inflation data, Federal Reserve policy, and any further global events that could impact interest rates. However, for now, this significant decrease in the 30-year fixed mortgage rate is something to celebrate and act upon if it aligns with your financial goals.

🏡 Two High‑Yield Rental Properties With Strong Cash Flow

Fort Wayne, IN

🏠 Property: Cinema Crossing

🛏️ Beds/Baths: 6 Bed • 5 Bath • 3012 sqft

💰 Price: $500,000 | Rent: $4,200

📊 Cap Rate: 7.0% | NOI: $2,920

📅 Year Built: 2026

📐 Price/Sq Ft: $167

🏙️ Neighborhood: B-

Port Charlotte, FL

🏠 Property: Arthur Ave

🛏️ Beds/Baths: 4 Bed • 2 Bath • 1914 sqft

💰 Price: $349,900 | Rent: $2,295

📊 Cap Rate: 5.6% | NOI: $1,633

📅 Year Built: 2025

📐 Price/Sq Ft: $183

🏙️ Neighborhood: A+

Indiana’s large 6‑bed rental with higher cap rate vs Florida’s new A+ property with stability. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Build Passive Income & Wealth with Turnkey Rentals

Mortgage rates remain near 6%, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

🔥 HOT INVESTMENT Properties JUST ADDED! 🔥

Request a Callback / Fill Out the Form Online

{kind=link}