")

At a Glance:

-

-

There are legit reasons to fear financial risks like asset bubbles, inflation, and geopolitical crises right now

-

I continue investing every month – while exploring contingencies

-

The day before Halloween, I find myself asking “What scares me right now?”

Here are a few things that jumped out at me:

-

Reheating inflation: since April’s 2.3% CPI reading, it’s climbed back above 3% last month

-

Asset bubbles: risk in stocks, AI & Big Tech, gold, and crypto

-

Risk of a 1929-style crash and depression that takes decades to recover from

-

Fraying geopolitical ties

-

Risk of political extremism leading to capital controls, soaring tax rates, or both

-

AI widening the opportunity gap so dramatically that it causes more polarization and higher taxes

Looking at all of those in the same place actually is spooking me a little. So let’s embrace the terror and explore these further.

Disclaimer

The information provided on this website is for general informational purposes only and should not be construed as legal, financial, or investment advice.

Always consult a licensed real estate consultant and/or financial advisor about your investment decisions.

Real estate investing involves risks; past performance does not indicate future results. We make no representations or warranties about the accuracy or reliability of the information provided.

Our articles may have affiliate links. If you click on an affiliate link, the affiliate may compensate our website at no cost to you. You can view our Privacy Policy here for more information.

Wealth Accumulation vs. Wealth Protection

For my entire adult life, I’ve focused on wealth accumulation. As you should in your 20s, 30s, and early 40s.

With economic and political storm clouds seemingly brewing on every horizon, I find myself starting to think a little more defensively.

How do I protect what I’ve built?

Don’t get me wrong, I continue investing in stocks on auto-pilot every week, and investing in passive real estate every month as a member of the Co-Investing Club.

But I also find myself asking “How would this investment hold up in an economic crash?”

The 4-Generation Cycle

Last year, I read a book called The Fourth Turning Is Here: What the Seasons of History Tell Us About How and When This Crisis Will End by historian Neil Howe. It makes the worrying case that every human civilization in history has experienced a four-generation cycle, culminating in an existential crisis that reshapes society and kicks off the next cycle.

Part of that has to do with building strong institutions in the midst and wake of the crisis, and those institutions gradually decaying over the next four generations.

The last of those crises in our civilization – the one-two punch of the Great Depression and World War II – happened four generations ago. And it definitely feels like there’s some electricity-in-the-air-before-the-storm today.

I do believe some type of crisis will hit in the next 3-7 years. A major war? An internal political revolution? Something painful and ugly, even it’s still too distant to see clearly now.

Whenever and whatever the next crisis is, I want to survive it with my wealth intact. But that’s easier said than done.

(article continues below)

Real estate investments? Awesome.

Being a landlord? Less fun.

Learn how to earn 15%+ on passive real estate investments in our free video course.

Contingencies for Economic Risk

What contingencies can you put in place to protect against the risk of a major crisis?

Most people jump to Treasury bonds as their first answer. I totally disagree, due to inflation risk. Don’t believe me? Consider the debt-to-GDP ratio in the US, which is in the not-so-esteemed company of Venezuela, Zambia, Greece, France, and Sudan. Governments have a playbook when their public debt gets too high: they inflate it away.

Another contingency option is gold, and I invested some money in it this past summer. But it’s exploded over 98.8% over the last two years, nearly doubling its previous all-time high.

That scares me. I’ll still put some more money in gold, but it feels a bit like an unsustainable bubble.

“Okay, what about real estate?”

Real estate can help. But it’s not foolproof: property prices can and do go down sometimes, especially in a major economic crash. Still, it offers a strong inflation hedge, and in time it always bounces back because it has intrinsic value and demand.

Then there’s geopolitical risk.

Contingencies for Geopolitical Risk

I spent ten years living abroad, and moved back to the States this year to be closer to family. Given the polarization in the US, I find myself asking “How could I protect my assets if the US became super authoritarian or socialistic?”

My initial response was just “Move back overseas.” But that’s not a complete answer.

I’ve had a series of conversations with my financial planner friend Carrie recently about this topic. They’ve gone something like this:

Me: “You can avoid authoritarianism by just leaving the country. You can’t avoid high taxes from socialism by doing so, because the US still taxes you regardless of where you live.”

Carrie: “That’s true. But taxes aren’t the only risk – there’s also the risk of capital controls. In either an authoritarian or socialist state, they could restrict access to your money. That could mean throttling how much you withdraw each month, or how much you can move overseas. Or they could nationalize private assets above a certain threshold, or some other scheme. In a worst case, they could physically prevent you from leaving the country too.”

Me: “Well that’s terrifying. Good thing I own plenty of international stock funds.”

Carrie: “That won’t help you, since you own funds on US stock exchanges in US accounts.”

Me: “F%#&. So what are you doing?”

Carrie: “Applying for a second residency in another country and moving some of my assets there.”

Scared yet?

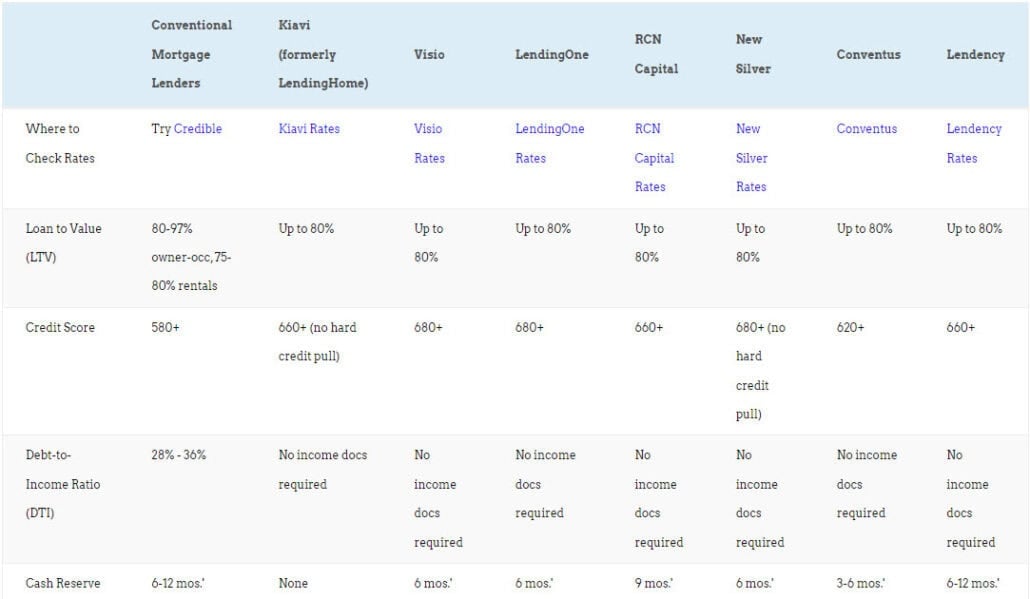

Want to compare investment property loans?

What do lenders charge for a rental property mortgage? What credit scores and down payments do they require?

How about fix-and-flip loans?

We compare the best purchase-rehab lenders and long-term landlord loans on LTV, interest rates, closing costs, income requirements and more.

Balancing Fear vs. Growth

Carrie and I were playing out worst-case scenarios as hypotheticals. Neither of us actually thinks the US will devolve into an authoritarian or socialist state.

Even so, after WWII the US imposed a 90% tax rate on higher earners. In the Great Depression, Uncle Sam implemented capital controls such as outlawing private citizens from owning gold and forcing them to sell it to the US government (at its own prices).

Economic crashes, soaring inflation, extreme tax rates, and capital controls have all happened – right here in the US. This isn’t sci-fi.

I continue investing every month in real estate and stocks. You have to balance the need to grow your portfolio against macroeconomic and political risks.

For further exploration of this topic, here’s an article I wrote for BiggerPockets last year about how different real estate assets would fare in another World War. It’s not as depressing as it sounds.

I’m still keeping my long-term residency in Brazil in good standing though. Just in case.

Want to talk about risk vs. growth further? Hop on the open Zoom call with Deni and me today at 3:30 EST.

Connect with us on social!

The post What Scares Me Right Now (Financially) appeared first on SparkRental.

{kind=link}