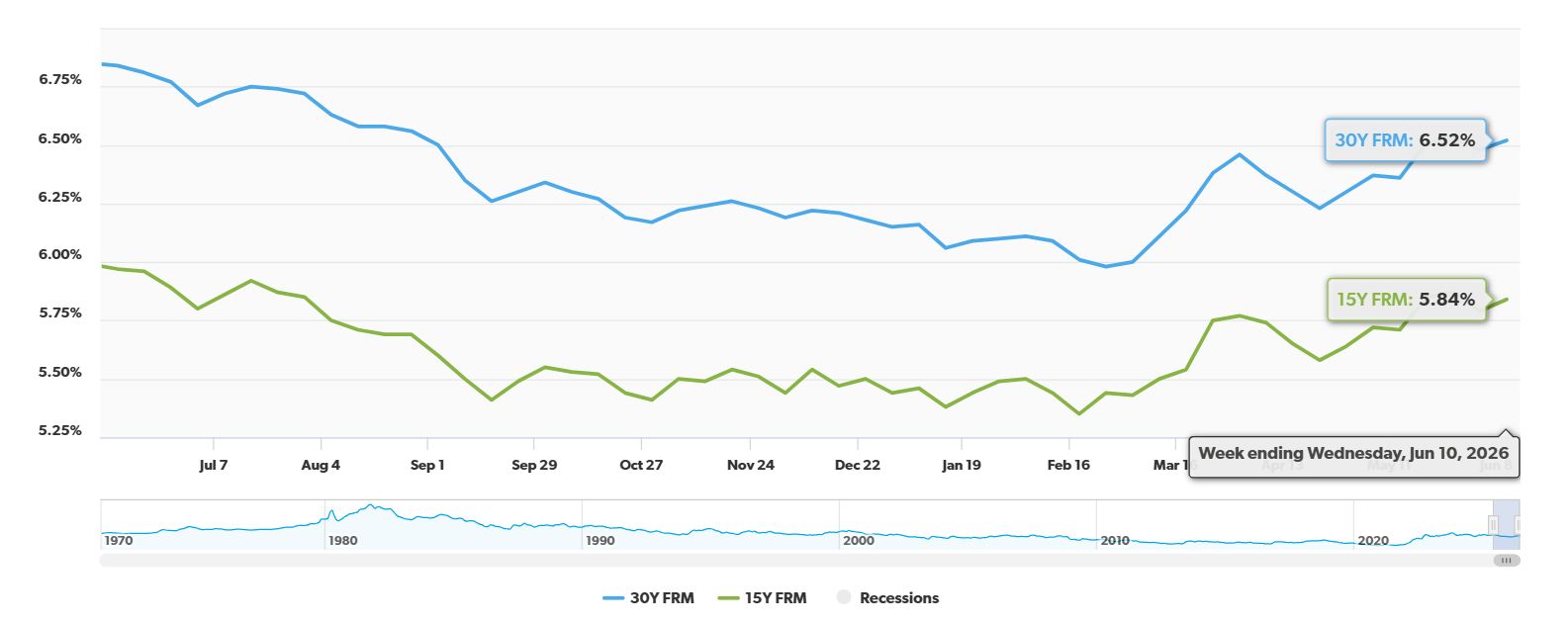

According to the Freddie Mac Primary Mortgage Market Survey for the week ending June 11, 2026, the 30-year fixed-rate mortgage averaged 6.52%, marking a 32-basis-point drop year-over-year from the 6.84% average recorded during the same week in 2025. While borrowing costs have trended lower over the past 12 months, rates ticked up slightly from last week’s average of 6.48% due to resilient labor data and sticky consumer inflation. This annual decrease translates into tangible savings for borrowers, making homeownership more attainable despite current economic pressures.

30-Year Fixed Mortgage Rate Drops by 32 Basis Points Year-Over-Year

Understanding the Numbers: A Closer Look at the Decline

Let’s break down what this means. Freddie Mac, a key player in the housing finance industry, releases weekly surveys that are a benchmark for mortgage rates across the country. Their data for the week ending June 11, 2026, shows the average 30-year fixed-rate mortgage at 6.52%.

Here’s a quick look at how this compares:

| Loan Type | Weekly Average (06/11/2026) | 1-Week Change | 1-Year Change |

|---|---|---|---|

| 30-Yr Fixed FRM | 6.52% | +0.04% | -0.32% |

| 15-Yr Fixed FRM | 5.84% | +0.05% | -0.13% |

FRM stands for Fixed-Rate Mortgage.

You can see the 30-year fixed rate is a full 0.32% lower than it was a year ago. This is a substantial move. While the weekly jump of 0.04% might seem small, it’s the year-over-year trend that truly signals a more affordable borrowing environment for many. The 15-year fixed-rate mortgage also saw a year-over-year decrease, though it wasn’t as pronounced.

Why the Slight Weekly Jump? Factors at Play

It’s important to understand that mortgage rates don’t move in a straight line. Even with the positive year-over-year trend, rates can fluctuate weekly. The data from Freddie Mac points to a couple of key reasons for the slight increase from last week:

- Resilient Labor Data: The latest jobs report showed more new jobs were created than economists predicted. This is generally a good sign for the economy, but it can also signal that the Federal Reserve might be less inclined to lower its benchmark interest rates quickly. Lower benchmark rates often lead to lower mortgage rates.

- Sticky Consumer Inflation: While inflation has cooled from its peak, it’s still proving to be a bit stubborn. When inflation is higher, it can put upward pressure on interest rates as lenders try to keep pace with rising costs.

These are the forces that are essentially creating a floor under mortgage rates, preventing them from plummeting back into the 5% range we saw in some more favorable periods.

The Real Impact: What a 32-Basis-Point Drop Means for Your Wallet

This is where it gets exciting for potential homeowners. A 32-basis-point reduction in your interest rate can make a significant difference in your monthly mortgage payment and the total interest you pay over the life of your loan.

Let’s imagine you’re looking at a standard $400,000, 30-year fixed loan.

- At 6.52%, your estimated monthly principal and interest payment would be around $2,533.54.

- If the rate were 6.20% (representing a 32-basis-point drop from the current 6.52%), that same loan’s monthly payment would be approximately $2,449.88.

That’s a monthly savings of $83.66!

Over the 30-year life of the loan, this translates to a total interest saving of $30,117.60. That’s money you can use for home improvements, savings, or simply enjoy.

Here’s a table showing how this drop impacts various loan amounts:

| Loan Amount | Monthly Payment at 6.52% | Monthly Payment at 6.20% | Monthly Savings | 30-Year Lifetime Savings |

|---|---|---|---|---|

| $300,000 | $1,900.16 | $1,837.41 | $62.75 | $22,590.00 |

| $400,000 | $2,533.54 | $2,449.88 | $83.66 | $30,117.60 |

| $500,000 | $3,166.93 | $3,062.35 | $104.58 | $37,648.80 |

| $600,000 | $3,800.31 | $3,674.82 | $125.49 | $45,176.40 |

Note: These are estimates for principal and interest only and do not include taxes, insurance, or fees.

What This Means for the Housing Market and Buyers

This annual rate reduction, even with slight weekly ups and downs, is a positive signal for the housing market. It boosts buyer purchasing power. For instance, Redfin data suggests that new home listings have surged, creating a more favorable inventory situation for buyers. With nearly 47% more sellers than active buyers in some areas, homebuyers might find they have more room to negotiate on price, even with mortgage rates in the mid-6% range.

From my perspective, this environment presents a unique opportunity. Buyers who have been patiently waiting for rates to dip may find that now is a good time to re-enter the market. The combination of a more favorable interest rate year-over-year and potentially increased inventory can lead to a better overall home-buying experience. It’s crucial, however, to stay informed about weekly rate changes and consult with a mortgage professional to understand how these fluctuations might affect your specific situation.

The average 30-year fixed mortgage rate falling by 32 basis points year-over-year to 6.52% is a clear indication of improving affordability for potential homebuyers, despite some ongoing economic factors keeping rates from falling further.

🏡 Out‑of‑State Real Estate Investment: Tennessee vs Florida

Franklin, TN

🏠 Property: Ribbon Ln

🛏️ Beds/Baths: 2 Bed • 2.5 Bath • 1662 sqft

💰 Price: $569,999 | Rent: $3,000

📊 Cap Rate: 5.1% | NOI: $2,415

📅 Year Built: 2022

📐 Price/Sq Ft: $343

🏙️ Neighborhood: A-

Port Charlotte, FL

🏠 Property: Chamberlain Blvd

🛏️ Beds/Baths: 4 Bed • 2 Bath • 1617 sqft

💰 Price: $274,900 | Rent: $1,845

📊 Cap Rate: 5.4% | NOI: $1,231

📅 Year Built: 2023

📐 Price/Sq Ft: $171

🏙️ Neighborhood: A+

Out‑of‑State investors can compare Tennessee’s newer rental with higher NOI vs Florida’s A+ property with strong yield. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Build Passive Income & Wealth with Turnkey Rentals

Mortgage rates remain near 6%, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

🔥 HOT INVESTMENT Properties JUST ADDED! 🔥

Request a Callback / Fill Out the Form Online

{kind=link}